Follow these simple guides once you have selected the “most” appropriate model. (1) Check the residuals correlogram to see if there’s any information yet to be captured in this model; (2) a flat correlogram is most ideal; (3) if a lag is significant, re-estimate the model; (4) check the residuals correlogram again; (5) but, avoid over-fitting a model; (6) perform Ljung-Box test for squared residuals (autocorrelation test).

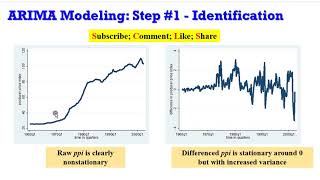

Always remember that the fundamental idea of the B-J methodology is that of parsimony (meagreness or stinginess); because parsimonious models produce better results than over-parameterised models. Too many variables in a model consumes degrees of freedom more so when those variables contribute little to the significance of the dependent variable; may result in negative adjusted R-squared. A flat correlogram of the residuals is most ideal and avoid “over-fitting” an ARIMA model to a data series. The forecast is based on the final ARIMA model and there cannot be an exact or perfect ARIMA model because it is more “of an art than of science”. How can the “most” appropriate model be estimated and selected from the tentative models identified? First, estimate all the tentative models and select the most appropriate using these criteria. Choose the model having (1) most significant coefficients (2) least volatility (3) highest adjusted R-squared (4) lowest AIC/SIC. Since, ARMA/ARIMA is a method among several used in forecasting variables, the tools required for identification are: correlogram, autocorrelation function and partial autocorrelation function. The partial autocorrelation (PAC) measures correlation between (time series) observations that are k time periods apart after controlling for correlations at intermediate lags (i.e., lags less than k). In other words, partial autocorrelation is the correlation between Yt and Yt−k after removing the effect of the intermediate Y’s (measures the marginal impact). To identify the appropriate ARMA/ARIMA model, I have outlines 5 procedures: (1) plot the series to visualise if stationary or not; (2) from the correlogram, calculate the ACF and PACF of the raw data. Check whether the series is stationary or not. If the series is stationary go to step 4, if not go to step 3; (3) take the first differences of the raw data and calculate the ACF and PACF from the correlogram; (4) visualise the graphs of the ACF and PACF and determine which models would be good starting points; and (5) estimate those models. Using EViews10, this video shows you how to perfrom diagnostics using the correlogram of the residuals. Here is the link to the Gujarati and Porter Ex21-1.wf1 dataset (EViews file) used for this tutorial http://cruncheconometrix.com.ng/datasets/gujarati-and-porter datasets-2/. Endeavour to have a Google account for easy accessibility.

Follow up with soft-notes and updates from CrunchEconometrix:

Website: http://cruncheconometrix.com.ng

Blog: https://cruncheconometrix.blogspot.com.ng/

Forum: http://cruncheconometrix.com.ng/blog/forum/

Facebook: https://www.facebook.com/CrunchEconometrix

YouTube Custom URL: https://www.youtube.com/c/CrunchEconometrix

Stata Videos Playlist:

https://www.youtube.com/watch?v=sTpeY31zcZs&list=PL92YnqQQ1gbjyoGWR2VUemNPU93yivXZx

EViews Videos Playlist:

https://www.youtube.com/watch?v=znObTs4aJA0&list=PL92YnqQQ1gbghRSJURtz08AZdImbge4h-

10:31

10:31

19:04

19:04

20:38

20:38

5:47

5:47

4:46:22

4:46:22

10:39

10:39

1:12:55

1:12:55

13:38

13:38

9:51

9:51

13:36

13:36

14:12

14:12

1:05:52

1:05:52

13:30

13:30

10:04

10:04

14:51

14:51

27:27

27:27

16:14

16:14

5:07

5:07

19:19

19:19