Level II CFA® Program Video Lessons offered by AnalystPrep

For Level II Practice Cases and Mock Exams: https://analystprep.com/shop/practice-package-for-level-ii-of-the-cfa-exam-by-analystprep/

For Level I Video Lessons, Study Notes, Question Bank, CBT Mock Exams & More: https://analystprep.com/shop/cfa-level-1-learn-practice-package/

For FRM (Part I & Part II) Video Lessons, Study Notes, Question Bank, CBT Mock Exams & More: https://analystprep.com/shop/unlimited-package-for-frm-part-i-part-ii/

Readings 6 – Times-series Analysis

0:00 Introduction and Learning Outcome Statements

1:24 LOS: Calculate and evaluate the predicted trend value for a time series, modeled as either a linear trend or a log-linear trend, given the estimated trend coefficients

5:45 LOS: Describe factors that determine whether a linear or a log-linear trend should be used with a particular time series and evaluate limitations of trend models

7:24 LOS: Explain the requirement for a time series to be covariance stationary and describe the significance of a series that is not stationary

8:45 LOS: Describe the structure of an autoregressive (AR) model of order p and calculate one- and two period-ahead forecasts given the estimated coefficients

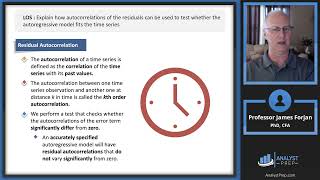

14:07 LOS: Explain how autocorrelations of the residuals can be used to test whether the autoregressive model fits the time series

18:58 LOS: Explain mean reversion and calculate a mean-reverting level

21:06 LOS: Contrast in-sample and out-of-sample forecasts and compare the forecasting accuracy of different time-series models based on the root mean squared error criterion

25:01 LOS: Explain the instability of coefficients of time-series models

27:30 LOS: Describe characteristics of random walk processes and contrast them to covariance stationary processes.

31:24 LOS: Describe implications of unit roots for time-series analysis, explain when unit-roots are likely to occur and how to test for them, and demonstrate how a time series with a unit root can be transformed so it can be analyzed with an AR model

33:25 LOS: Describe the steps of the unit root test for non-stationary and explain the relation of the test to autoregressive time-series models

36:49 LOS: Explain how to test and correct for seasonality in a time-series model and calculate and interpret a forecasted value using an AR model with a seasonal lag

42:35 LOS: Explain autoregressive conditional heteroskedasticity (ARCH) and describe how ARCH models can be applied to predict the variance of a time series

46:59 LOS: Explain how time-series variables should be analyzed for nonstationary and/or cointegration before use in linear regression

53:27 LOS: Determine an appropriate time-series model to analyze a given investment problem and justify that choice

55:02

55:02

4:46:22

4:46:22

1:22:32

1:22:32

18:36

18:36

27:59

27:59

![Upbeat Lofi - Deep Focus & Energy for Work [R&B, Neo Soul, Lofi Hiphop]](https://i.ytimg.com/vi/THh4fT0O7IY/mqdefault.jpg) 3:22:29

3:22:29

53:27

53:27

20:38

20:38

53:07

53:07

48:37

48:37

45:37

45:37

51:48

51:48

52:17

52:17

41:45

41:45

1:07:10

1:07:10

38:42

38:42

42:54

42:54

21:38

21:38

19:34

19:34

44:38

44:38