Session 6B: Monte Carlo Simulations in Finance & Investing

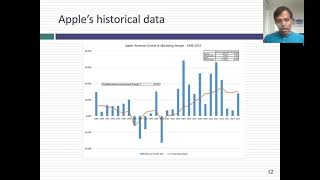

Monte Carlo simulations allow us to face up to uncertainty, rather than hide from it. In this session, I describe the steps in a simulation, starting with choosing the input variables that you will be using probability distributions (rather than point estimates), moving on to choosing the right distributions & parameters for these variables, ending with a reading of what the simulation output tells us about the output variable. I use a valuation of Apple from 2016 to illustrate the process.

Slides: http://www.stern.nyu.edu/~adamodar/pdfiles/Statistics101/Slides/Session6B.pdf

Post class test: http://www.stern.nyu.edu/~adamodar/pdfiles/Statistics101/postclass/session6Btest.pdf

Post class test solution: http://www.stern.nyu.edu/~adamodar/pdfiles/Statistics101/postclass/session6Bsoln.pdf

Webpage for statistics class: http://people.stern.nyu.edu/adamodar/New_Home_Page/webcaststatistics.htm

YouTube Playlist for this class: https://www.youtube.com/playlist?list=PLUkh9m2BorqmXcRzWFbzcjMd7fYErVexF