ERPEM 2014 - "High Dimensional Estimation: from foundations to Econometric models" - Aula 01

ERPEM 2014 - Minicourse: "High Dimensional Estimation: from foundations to Econometric models"

Professor: Alexandre Belloni

Aula 01 - 10/11/2014

Página: http://www.impa.br/opencms/en/eventos/store_old/evento_1412

Download dos vídeos:

http://video.impa.br/index.php?page=erpem-2014

Abstract:

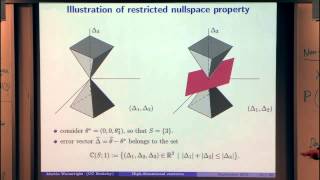

In this mini-course we start with the foundations of modern statistical techniques based on L1-penalization for high dimensional estimation under sparsity assumptions. We will cover rates of convergence for Lasso, sparsity bounds on the selected model, and simple lower bounds on its performance. We then will shift our interests to how further develop these ideas on models that are motivated by Econometric applications. For example, heteroskedastic errors, logistic regression, conditional quantiles, and error-in-variables. Some emphasis will be placed on properly handling the different assumptions induced by the (econometric) data generating process (e.g. approximate sparse models and non- Gaussian errors). We will finish the mini-course by establishing results on the uniform validity of confidence regions (e.g. confidence intervals) for parameters. We will attempt to cover partially linear models, instrumental variables, and Z-estimators.

IMPA - Instituto Nacional de Matemática Pura e Aplicada ©

http://www.impa.br | http://video.impa.br

Os direitos sobre todo o material deste canal pertencem ao Instituto de Matemática Pura e Aplicada, sendo vedada a utilização total ou parcial do conteúdo sem autorização prévia e por escrito do referido titular, salvo nas hipóteses previstas na legislação vigente.

The rights over all the material in this channel belong to the Instituto de Matemática Pura e Aplicada, and it is forbidden to use all or part of it without prior written authorization from the above mentioned holder, except in the cases prescribed in the current legislation.

52:26

52:26

2:05:54

2:05:54

1:30:15

1:30:15

1:08:33

1:08:33

34:21

34:21

1:11:24

1:11:24

4:00:37

4:00:37

43:22

43:22

9:08:53

9:08:53

21:14

21:14

2:14:39

2:14:39

17:54

17:54

3:24:55

3:24:55

3:52:07

3:52:07

58:02

58:02

1:17:41

1:17:41

12:45

12:45

2:10:25

2:10:25

3:22:17

3:22:17

37:46

37:46